News & information

Poor Joe Corbett. The Postal Service’s chief financial officer probably finds it hard to get out of bed each morning, knowing that his bank account holds only a fraction of what he owes on his home mortgage, car loan and credit cards. Then he has to go to work at the Postal Service and face, what he thinks, are the same daunting financial circumstances.

Of course, most Americans—geniuses or otherwise—know that comparing your total liabilities over the next several decades to a small fraction of your assets that’s held in cash is probably not the right way to approach the problem.

Kidding aside, Corbett, who was interviewed for a Wall Street Journal online edition blog post, knows perfectly well that he’s blowing smoke. The chart that he provided The Journal, comparing the Postal Service’s “total liabilities” to its current and projected cash balance, is designed to bamboozle readers into buying USPS’ plan to continue to dismantle the nation’s invaluable postal networks.

CFOs of major companies don’t compare their liabilities to their companies’ cash balances. Rather they compare total liabilities to total assets.

This bogus comparison was designed to convince Journal readers that the USPS is near collapse and that its radical downsizing is in order. Corbett has been peddling this misleadingly selective liabilities chart for months to convince Congress that it’s time to radically slash services to the tens of millions of American businesses and households that rely on the Postal Service to conduct business and to communicate every day.

USPS wants to end Saturday delivery and phase out door delivery to tens of millions of homes and businesses, in favor of cluster boxes. We think there is a much better way. We need fundamental reform to dramatically reduce the pre-funding burden, change how the retiree health fund is invested, improve USPS’ pension valuations, and modernize our pricing and new-product regulations.

So, let’s set the record straight.

Yes, the U.S. Postal Service’s financial situation is fragile, thanks mostly to Congress, which imposed a crushing mandate on USPS in 2006 to pre-fund decades' worth of future retiree health premiums over the past seven and a half years. Indeed, 83 percent of the $47 billion in USPS losses since 2007 are due to the pre-funding expenses, a burden no other company in America faces.

And although the Postal Service’s $4 billion cash balance is dangerously low, it’s up dramatically from its level of $1 billion in 2011.

That’s because the Postal Service has bounced back from the Great Recession. As the economy has slowly rebounded, USPS has recovered on the strength of booming e-commerce deliveries and growing advertising volume, which have more than offset the decline in First Class Mail due to Internet diversion.

Indeed, over the first two quarters of 2014, package revenue growth of $730 million strongly outpaced the $230 million decline in letter mail revenue.

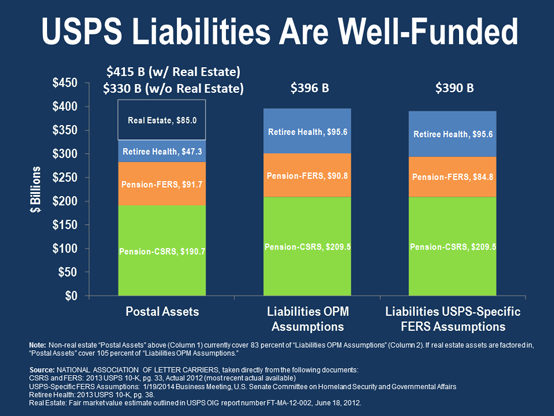

If the Postal Service wanted to have an honest discussion of liabilities, it would not just show unfunded liabilities marked to market with current interest rates. Nor would it ignore its assets, similarly marked to market.

The NALC chart above offers a more accurate picture of the Postal Service’s assets and liabilities. Although the chart leaves out workers’ compensation liabilities, which have been temporarily inflated due to record low interest rates, it shows that the Postal Service’s pensions are nearly fully funded and that the USPS has pre-funded a much greater share of future retiree health benefits than most, if not all, Fortune 1000 companies. Indeed, two-thirds of such companies don’t pre-fund retiree health benefits at all.

The NALC chart also shows that, with its real estate carried at market value, the Postal Service’s overall financial picture is stronger than Corbett tried to suggest with the chart he provided The Journal.

Indeed, if the Postal Service or the Office of Personnel Management were allowed to invest USPS’ $290 billion retiree pension fund and its $47 billion retiree health fund in a safe mix of long-term index funds offered by the federal Thrift Savings Plan, the Postal Service’s liabilities would be massively over-funded. (Under current law, these funds must be invested in low-yielding Treasury securities.)

We doubt many of The Journal’s sophisticated readers or writers fell for what Corbett was peddling. But the Postal Service clearly hopes Congress will.